Introducing a tax on agricultural GHG emissions? The Danish Case

Denmark is the first EU country with a proposal for GHG emission pricing in the agriculture sector. Such plans were requested in a progress report on EU climate policy, published in January 2024, by the newly-established European Scientific Advisory Board on Climate Change. They noted that there is no EU-level price on emissions in the agriculture and foodsectors, forestry and land use, which suffer from an overall lack of incentives to reduce emissions and increase removals. It recommended that the EU should start preparations now with a view to expanding the pricing regime of EU GHG emissions to all major emitting sectors, including agricultural/food and LULUCF, through a legislative proposal for after 2030. The EU Commission willl present new plans for studying options for a new Emission Trading Scheme for the agriculture sector during a conference 19th June.

In November 2023 the EU Commission published an exploratory study investigating ways to price GHG emissions from agricultural activities along the agri-food value chain and how this could be accompanied by providing farmers and other landowners with financial incentives for climate action. The study responded to a 2021 report by the European Court of Auditors, which recommended that the Commission should “assess the potential of applying the polluter-pays principle to agricultural emissions, and reward farmers for long-term carbon removals”. The study looked at different models for an emissions trading scheme that might incentivise emission reductions in agriculture (AgETS) identifying their advantages and drawbacks. The Commission plans further work to examine the issues raised in greater detail. These activities will continue till spring 2025, with an EU Commission proposal for an AgETS planned for 2026.

To date, only in New Zealand has serious consideration been given to the design of a system to price agricultural emissions, but implementation has been delayed on successive occasions. It is now possible that Denmark will become the frontrunner in introducing a pricing system for agricultural emissions. The current government has pledged to introduce a carbon tax on agricultural emissions and commissioned an Expert Group to recommend how this might be done. The Expert Group delivered its report in February 2024 and the government has asked a tripartite commission to come forward with a concrete proposal based on its recommendations by June 2024. The political decision will be taken after the summerbreak.

The Expert Group report is available in English. We first describe the challenge in meeting the Danish government’s ambitious 2030 climate target and the essential requirement to reduce agricultural emissions if its target is to be reached. Then, the main findings of the Expert Group will be summarized as they clearly have important lessons for the ongoing discussion in the EU.

Denmark’s climate targets in agriculture

The programme for government of the new Danish government formed in December 2022 Ansvar for Danmark (Responsibility for Denmark) recognised that climate change, together with the nature and biodiversity crisis, was the biggest challenge for this generation. It proposed to bring forward the date to achieve net zero GHG emissions from 2050 to 2045 and to set a new target of a 110% reduction in net emissions in 2050 compared to the 1990 figure. It confirmed the Danish emissions reduction target of 70% by 2030 compared to 1990 and the corresponding milestone of 50-54% reduction by 2025, while noting that it would evaluate whether this target should be strengthened further (these targets are measured over a three-year period centred on these dates).

It noted that achieving the existing 70% reduction goal would require the realisation of the binding reduction target of 55-65% relative to 1990 agreed by nearly all political parties in Parliament in the national agricultural agreement (“Landbrugsaftale”) for the combined agricultural and forestry sectors in October 2021. This agreement was based on the figures for agricultural and LULUCF net emissions (combined referred to as AFOLU emissions in this post) in the emissions projections published in 2021 (Klimafremskrivning 21 or KF21).

In those projections, AFOLU emissions in 1990 (excluding energy use) were 19.6 million tonnes (Mt) CO2e in 1990, so the target 2030 emissions amounted to between 6.9 and 8.8 Mt CO2e. On a ‘with existing measures’ basis, AFOLU emissions in 2030 were projected in 2021 to be 14.9 Mt CO2e, compared to 2019 emissions of 13.5 Mt CO2e (the increase was made up of a projected reduction in agricultural emissions which was more than offset by a switch in the forestry sector from being a net sink to a net source of emissions). This gave a reduction gap to be eliminated of between 6.1 and 8.0 Mt CO2e. The parties to the agricultural agreement stated their common ambition that greenhouse gas emissions for the agricultural and forestry sector will be reduced by 8 Mt CO2e in 2030 compared to BAU projections. Achieving this reduction should take account of the principles of the Climate Act, including sustainable business development and Danish competitiveness, sound public finances and employment.

In practice, the agreement proposed to reduce emissions by 7.4 Mt CO2e in 2030 relative to BAU projections, or a 50% reduction in AFOLU emissions over a period of 11 years. This proposed scale of ambition was still extraordinary exceeding that of any other EU Member State (Ireland, for example, which also has an ambitious target proposes to reduce emissions from agriculture alone by 25% between 2018 and 2030, while it still must set a target for LULUCF emissions).

Measures to achieve this 7.4 Mt CO2e reduction were set out in the agreement. 2.4 Mt CO2e were covered by an ‘implementation’ track and a further 5 Mt CO2e were covered by a ‘development’ track. The implementation track consisted of initiatives either in place or agreed as part of the agriculture agreement. The development track was a more speculative ‘black box’ of potential interventions for which considerable funding was set aside for research and development. The agreement provided that within the following year a strategy should be drawn up to concretise the reductions foreseen in the development track and to move these where possible to the implementation track.

Among the many elements of the 2021 Danish agriculture agreement was that it recognised that “The future regulation of agricultural emissions of greenhouse gases and nutrients must be based to a greater extent on farm-level inventories of the emissions. It can ensure more targeted and cost-effective efforts (my translation).” The parties to the agreement agreed to set aside DKK 249 (EUR 33.2) million to initiate research and development of farm carbon accounts and improved mapping for a new regulatory model.

This element must be seen in the context of the agreement on a green tax reform agreed by the Danish Parliament in December 2020. This agreement established that a uniform carbon tax should be a central instrument to achieve the 70% reduction target by 2030 but recognised that more work was needed to design an appropriate regime. The government established an Expert Group on Green Tax Reform in February 2021 with the brief to design a more uniform carbon pricing regime for all emissions as the most economically-efficient instrument to achieve the Danish reduction target of 70% relative to 1990, while taking account of other principles in the Danish Climate Law such as minimizing adverse competitiveness and leakage effects, be fiscally neutral, be socially balanced, and administratively feasible. The terms of reference for this committee required it to produce two reports. The first report was concerned with the rebalancing of taxes and levies mainly on energy and industry, while the second report should address the regulation of emissions from the remaining sectors and especially agriculture and LULUCF. This specific task was outlined as follows:

“The second partial report must also contain an assessment of the advantages and disadvantages of a regulatory solution for the agricultural sector, a subsidy solution within the EU’s agricultural support and a CO2e tax for this sector or a combination of these, as well as possible measures for cost-effective regulation of agriculture, which addresses CO2e emissions and other externalities, including e.g. environment and health. Farm accounts are a prerequisite for CO2e taxes on agriculture. It is assumed that the work in this regard will proceed under separate auspices. In addition, an assessment of the advantages and disadvantages of different solutions for emissions from agricultural land and other emissions from LULUCF must be included, which the expert group deems relevant to elucidate. Consideration must be given to upcoming EU legislation in the area, including a potential new approach to regulating agriculture’s climate impact through revision of the burden sharing agreement and the LULUCF regulation in the EU and a separate agricultural pillar in the EU’s quota system”.

The Expert Group, also called the Svarer Committee after its chairperson the economist Michael Svarer, published the first of its two reports in February 2022 addressing taxation of energy and industry. The Committee concluded that it was impossible to reconcile all objectives set out in the Climate Law. It proposed different models which weighted economic efficiency, leakage effects and impact on the public finances differently, leaving it to politicians to make the final choice. This was quickly followed by a political agreement in June 2022 to introduce a uniform CO2 tax of DKK 750 (€100)/t CO2e on emissions from all industries not covered by the EU Emissions Trading Scheme (ETS), DKK 375 (€50)/t for industries covered by the EU ETS (in addition to the ETS allowance price), and DKK125 (€16.7)/t for mineralogical processes (e.g. cement) in addition to the ETS allowance price. These carbon taxes should be phased in from 2025 to 2030. This political decision was in line with the Committee’s recommendation that a uniform tax across all industries would be the economically most cost-effective design but that it needed to be modified to account for potential competitiveness and leakage impacts.

The Committee had already begun work on its second report, to cover emissions in the agriculture and forestry sectors, when there was a change in government in December 2022. The previous government had been a minority Social Democratic government. The new government was a coalition of parties from the centre-right (the Liberal Party), the centre (Moderates) and the centre-left (Social Democrats). A key issue for decision in the programme for government was the new government’s attitude to the prospect of the pricing of agricultural emissions. This was a tricky issue in particular for the Liberal Party which traditionally has been the voice of farm interests. The programme for government was nonetheless clear that:

“The government will present a proposal for a climate tax on agriculture when the Expert Group for a Green tax reform has presented its conclusions. The climate tax must ensure implementation of the development track and fulfilment of the binding reduction target for the agricultural and forestry sector of 55-65 per cent in 2030 compared to 1990. The government will ask the expert committee to present different scenarios to achieve this goal in line with the recommendations the committee presented in connection with the CO2e tax on industry, including consideration of countering the relocation of production, incorporating international experience and the possibility of imposing a CO2e tax on final consumption as a possible means of action”.

This addition to the Expert Group’s terms of reference in the programme for government both narrowed the scope of the Expert Group’s work (by asking it to link its future recommendations for agriculture and land use to the recommendations it had already given for industry) but also extended it by asking it to examine a tax on final food consumption (e.g. meat) as a further potential instrument.

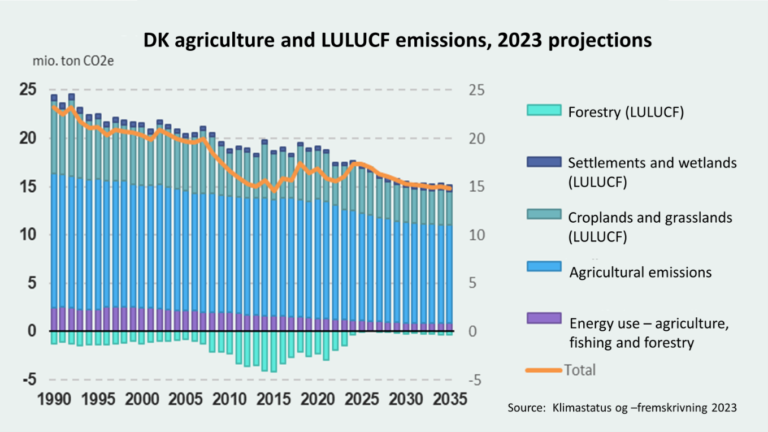

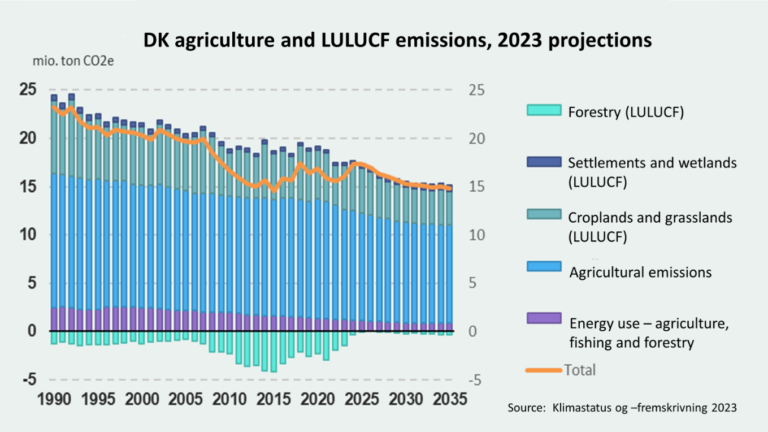

Before getting into the specifics of the Expert Group’s recommendations, these build on a modified version of the latest set of official GHG projections produced in 2023 (KF23) (see Figure 1) which have different implications for the reductions required in the AFOLU sector compared to those that underlay the 2021 agriculture agreement. There are two important adjustments.

figure 1. Danish agricultural and LULUCF emissions (including energy use), 1990-2035.

First, the Expert Group notes that the overall gap between projected 2030 total emissions and the 70% reduction target has been reduced by additional measures taken since 2021, such as the revised ETS Directive, a political agreement on green aviation, and higher diesel taxes. These additional measures take some of the pressure off finding reductions in the AFOLU sector. Until now, however, the reduction targets in the 2021 agricultural agreement have not been revised and were indeed re-affirmed in the programme for government in December 2022.

In addition, AFOLU non-energy related emissions in 2021 are now estimated at 11.8 Mt CO2e compared to 13.7 Mt CO2e in the KF21 projections produced in 2021. Projected 2030 non-energy related AFOLU emissions on a BAU basis are now 12.4 Mt CO2e rather than 14.9 Mt CO2e previously (and 14.4 Mt CO2e shown in the 2023 projections in Figure 1). One reason for the significant reduction over two years is new, lower, estimates of emissions from organic soils of 2 Mt CO2e which significantly reduces the remaining reductions needed from the AFOLU sector.

The Expert Group made its own calculation of the reduction gap that needed to be closed in the light of the new information. It calculated that the reduction gap for the AFOLU sector was now reduced to 2.5 Mt CO2e (the Danish Climate Council in its most recent Status Report 2024 published at the same time came to a similar reduction gap of 2.6 Mt CO2e). It estimates that phasing in a carbon tax from 2027 at the levels it proposes, together with subsidies for afforestation and re-wetting of organic soils, can reduce AFOLU emissions by 2.4-3.2 Mt CO2e by 2030 (and by more in later years as the sink due to afforestation increases as the young trees mature). In its view, this will allow Denmark to achieve its overall 2030 goal of a 70% reduction in net emissions while also fulfilling Denmark’s obligations under the EU Effort Sharing Regulation and the LULUCF Regulation.

The Expert Group proposals for a GHG emission tax for agriculture and subsidies

The starting point for the Expert Group’s recommendations is that the regulation of agricultural and land use emissions should be as close as possible to the approach taken to address energy and industrial emissions, avoiding as far as possible arbitrary differential treatment. Three different models are proposed, each of which weigh the criteria set out as the basis for climate policy in the Danish Climate Law differently. Before we present the three models, we first clarify (a) the emissions that would be covered by the carbon tax, and (b) the complementary measures that are common to all three models.

The proposed tax base would cover emissions from livestock (both from enteric fermentation and manure management), from fertiliser and lime applied to agricultural soils, and emissions from organic soils. The Expert Group explicitly did not recommend immediate inclusion of soil carbon sequestration due to gradually diminishing impact over time and the risks of reversibility. It also excluded nitrous oxide emissions from the return of crop residues to the soil, as well as indirect N2O emissions from fertiliser use. In total, the proposed tax base would cover 85% of the emissions included in the national inventory.

Also, forestry and forest management are not included in the tax base. However, as a complementary measure the Group recommends a significant increase in the afforestation subsidy to DKK92,000 (EUR12,666) per ha equivalent to a subsidy of DKK460/t CO2e (EUR 61.3/t) to increase planting to reach the government target of 250,000 ha of new forest by 2030. The climate benefits of afforestation are limited in the years to 2030 but become more significant post 2030.

For organic soils, all three models propose a very limited levy of DKK10/t CO2e (EUR1.33/t) together with a significant compensation payment to farmers who agree to rewet these soils. The combination of levy and subsidy is intended to provide an incentive for rewetting, which is seen as the only effective way to reduce emissions from these soils. The Group proposes that the size of the levy should be revisited in 2027 if it proves insufficient to meet the target (rewetting of 37,000 ha including previous initiatives in 2030).

Finally, there is a common levy of DKK750/t CO2e (EUR 100/t) on all F-gas emissions (mainly from refrigeration), corresponding to the levy imposed on these gases in other sectors.

Carbon tax vs. emissions trading

The Expert Group considered whether to recommend a carbon tax or an emissions trading scheme for agricultural emissions but decided against a trading scheme. It identified the main advantages of a trading scheme as being the ability to target a precise reduction in emissions and to reduce the burden on agriculture by granting free allowances (though it noted that it was possible to achieve a similar alleviation in a carbon tax regime through a system of rebates).

It listed several disadvantages of a trading scheme. One is uncertainty around the price imposed on emissions, particularly if there is a political desire to have a uniform price on emissions across sectors (the Expert Group recognised that this objection would have less weight if there were a desire to have a differential and exceptional treatment of agricultural emissions). Another is that volatility in allowance prices would create uncertainty around the profitability of investments designed to reduce emissions, so that the incentive to invest in new techniques is weakened in contrast to carbon taxes which are known in advance. It also concluded that it can be difficult to design a system of free allowances that does not discriminate between existing and future generations of farmers or that does not reduce the incentive to reduce emissions. The Expert Group did not discuss the mechanics of how a trading scheme might work where individual farms are the point of obligation which can also be problematic. Despite the technical arguments in favour of a carbon tax, the decisive argument for the Expert Group to choose this option may have been the requirement in its terms of reference to design a pricing scheme that was as close as possible to that introduced for the rest of the economy.

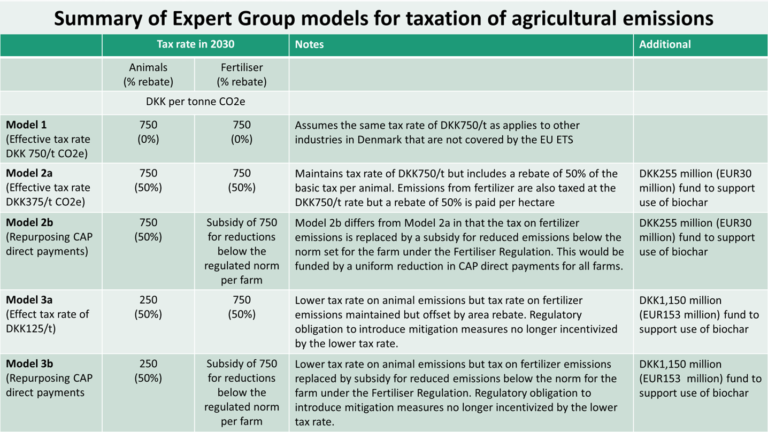

The three models

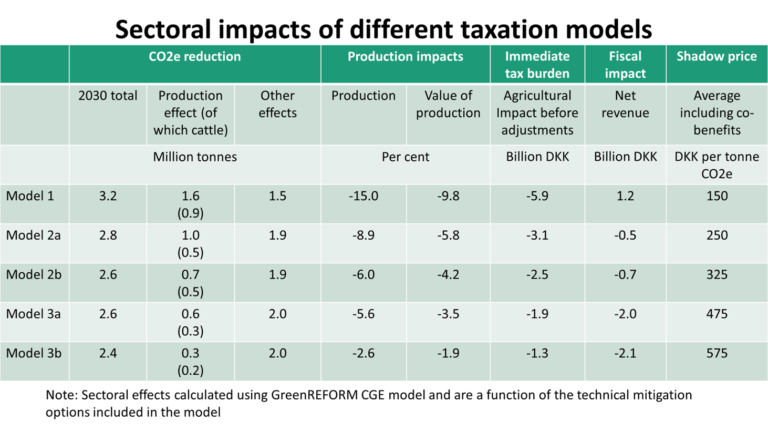

The three basic models proposed by the Expert Group (with two additional variants) are summarised in Table 1. In addition, all models are accompanied by the complementary measures related to afforestation, rewetting of organic soils, and F-gases.

Table 1. Expert Group models for taxation of agricultural non-CO2 emissions

Source: Own construction, based on Expert Group on Green Tax Reform, final report, February 2024.

The most ambitious model is Model 1, which would impose the same tax rate on all covered agricultural emissions as paid by other Danish industries not covered by the EU Emissions Trading Scheme. Model 2a would reduce the tax payable by half by introducing rebates (a fixed amount per animal for animal emissions, and a fixed amount per hectare for fertiliser emissions). The rate of DKK375/t CO2e corresponds to the tax payable by other Danish industries that are covered by the EU ETS. This model reduces the total tax payable but maintains the marginal incentive effect. If an individual farmer increases emissions per animal (e.g., by feeding additional concentrates to get a higher milk yield) the additional emissions will be taxed at the full marginal rate. If a farmer uses a feed additive that reduces emissions, he or she will benefit from a saving of DKK750/t on those reduced emissions.

In Model 3a the effective tax rate on animal emissions is further reduced to equal the tax rate paid by particularly sensitive industries (e.g. cement) of DKK125/t CO2e. The tax rate on emissions from spreading fertilizer is maintained at the same level as in Model 2a. The Group recognises that the lower tax rate for animal emissions means that there will not be a sufficient incentive for livestock farmers to adopt relevant emissions reduction technologies. It therefore proposes that Model 3 would be accompanied by regulatory requirements to ensure adoption of measures such as feed additives or covering manure storage tanks.

In Models 2b and 3b, the tax on emissions from fertiliser spreading is replaced by a subsidy for reductions in emissions below those that would arise from the fertiliser use norms permitted under the Fertiliser Regulation. Each year the Danish authorities calculate a maximum fertiliser quota for each holding based on the economically optimal fertiliser use for the farm’s cropping pattern in that year, taking account of factors such as its soil type and the average rainfall in the municipality where the farm is located. In these models, the full DKK750/t would be paid for reduced emissions below those that would arise from the maximum fertiliser quota. To ensure a neutral impact on the public finances, the Group proposes to fund this subsidy by a uniform reduction in area-based direct payments under the CAP for all farms.

To ensure that the target reductions in CO2e emissions are achieved in Models 2 and 3 with the lower tax rates, the Expert Group foresees in addition a state fund that would promote and support the use of biochar. Biochar uptake plays a particularly important role in Model 3 where it is assumed to contribute one-quarter (0.8 Mt CO2e) of the overall reduction of 2.4 Mt CO2e in that scenario by 2030. The Expert Group itself is doubtful whether sufficient pyrolysis capacity will be available to ensure a sufficient supply of biochar to meet this target. It also notes environmental approval for the use of biochar has yet to be given, so there is particular uncertainty around achieving the reduction targets in both variants of Model 3.

A consumption tax on meat?

We noted previously that the incoming government’s programme enlarged the terms of the reference for the Expert Group to also examine the case for introducing a tax on final consumption (eg meat). The Danish minister of Finance already made remarks on the option of a tax on beef, since beef has the highest GHG emission per kg meat compared to pork or chicken meat. The principal argument for placing the tax on final consumption is that domestically produced and imported products are treated similarly, there is no loss of competitiveness for domestic production and therefore no risk of carbon leakage. The Group assumed that a climate tax would be limited to the most emissions-intensive products, namely, beef, pigmeat and dairy products, and would reflect total emissions along the supply chain. Even though emissions associated with imported products would likely be different, the Group assumed that to be compliant with WTO rules the same tax would apply as for Danish products. Exports of Danish products would not be subject to the (consumer)tax.

The Expert Group concluded that a consumption tax would be much less effective at reducing Danish territorial emissions than a production tax. Partly this is because Danish consumption is much smaller than Danish production of these emissions-intensive products, and partly because a consumption tax does not give a direct incentive to individual farmers to change their practices (the products of farmers who adopt mitigation technologies would still be taxed at the same rate as the products of other farmers). The Group calculated that, to give the same reduction in Danish emissions introducing a consumption tax of DKK750/t CO2e would only allow the production tax to be reduced from DKK750 to DKK700/t CO2e. For these reasons the Expert Group did not recommend the introduction of an emissions tax on consumption.

However, the Danish Climate Council advised the Danish government to tax beef and dairy consumption too.

Implementation

Implementation of the proposed emissions tax would be based on farm-level carbon budgets (recall that funding was included in the 2021 agricultural agreement to prepare for these budgets). The emissions tax (and subsidy, where relevant) would be calculated based on the level of particular activities on individual farms multiplied by the emissions factor for these activities used in constructing the national inventory. The one exception is the levy on lime which would be paid by producers and importers. This approach ensures consistency between the aggregate of farm level budgets and national targets which are established based on the inventory figures. It requires that the inventory is sufficiently granular to differentiate between emissions from different types of animals, different manure management systems, different stable arrangements, and so on. Currently, the Danish national inventory recognises 250 different activities in its agricultural inventory. The report also recognised that the introduction of new technologies should be reflected in changed emission factors. An important benefit of the system will be the dynamic established to ensure that changes that farmers introduce in their practices that reduce emissions will be credited in the national inventory.

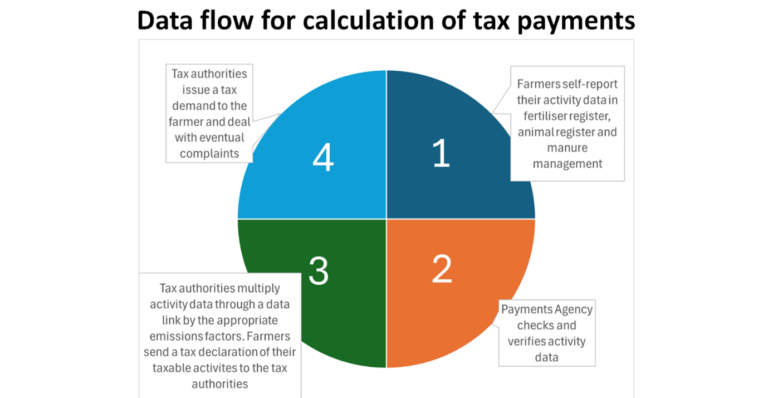

Administration of the tax will rely on close cooperation between the Ministry for Agriculture agency responsible for CAP payments and the maintenance of land parcel, animal and fertiliser registers, and the tax authorities. The Expert Group highlights that much of the necessary activity is already collected and held by the payments agency, with only minimal need for additional information. The proposed data flow is shown in Figure 2. Steps 1 and 2 are already implemented for CAP purposes, while Steps 3 and 4 would be new. A data link would be established between the payments agency and the tax authorities. The latter would multiply the activity data by the appropriate emission factors and issue a tax demand to the individual farmer. A farmer would have a right to appeal and disputes over the correctness of the tax demand would be settled in the usual way.

Figure 2. Illustration of data flow for implementation of proposed agricultural emissions tax.

Source: Expert Group on Green Tax Reform, final report, February 2024.

Economic and sectoral consequences

The economic and sectoral consequences of the different models are summarised in Table 2. These have been calculated using a specially-developed computable general equilibrium model called GreenReform. The first point to note is that, in going from the most ambitious Model 1 to the least ambitious Model 3b (measured in terms of emission reductions), there is a trade-off between the size of the reduction achieved and the immediate cost to the agricultural sector measured as the tax bill it would pay. The immediate tax burden is defined as the size of the tax bill before changes in markets (changes in prices of outputs and inputs) and farmers’ responses to the tax are factored in. It is calculated as the product of the sector’s CO2e emissions in 2030 and the rate of tax.

Table 2. Emission reduction and economic impacts of the different taxation models

Source: Expert Group on Green Tax Reform, final report, February 2024.

Whereas Model 1 is estimated to achieve a reduction of 3.2 Mt CO2e, this reduces to 2.4 Mt CO2e in Model 3b. On the other hand, the immediate tax burden on the agricultural sector of Model 3b is less than a quarter of that in Model 1. The final tax bill will be significantly less than the amounts shown in this table when farms, producer prices and the prices of inputs have adapted to the tax/subsidy, also taking account of any reduction in the volume of production. Estimates of the final tax bill as calculated in the Svarer report in the various model scenarios are presented later in the post.

Table 2 also shows the likely impact on Danish agricultural production of introducing the different models. For the most ambitious Model 1, the Expert Group expects a fall in the volume of production by 15%. An important mechanism in the GreenReform model that contributes to this result is an upward-sloping supply curve of land to the agricultural sector. This implies that, as the return to land in agricultural use decreases as a result of the tax, some land moves out of agricultural production into alternative uses (which could be forestry or ecological services or just left idle).

The Expert Group expects a smaller fall in the value of production by 9.8%. This is because the model assumes that part of the tax on production can be shifted forward to processors and final consumers so that output prices increase. We will see later that this is a controversial element in the Expert Group report as the industry claims that its ability to charge higher prices, particularly in export markets, simply because a climate tax has been introduced in Denmark is significantly overstated in the model. These production effects are greatly mitigated in the less ambitious models, which of course is precisely their objective.

The different models can also be compared with respect to their costs to the whole society by looking at their shadow price (the last column in Table 2). The shadow price indicates the average socio-economic cost per tonne CO2e reduction. It is a measure of the loss of economic well-being resulting from the increase in costs due to the introduction of the carbon tax. However, the shadow price has been adjusted to reflect the most important environmental side benefits arising from the tax (in addition to the gain from the CO2e reduction itself). Specifically, the shadow price is reduced by the health benefits of lower ammonia emissions, the recreational value of increased forest areas, as well as the reduced cost of meeting the EU’s requirements for water quality resulting from lower nitrogen leaching. The report recognises that rewetting organic soils may also have a positive impact on biodiversity but could not find a satisfactory way to include this.

We observe that, moving from the most ambitious Model 1 to the least ambitious Model 3b, the immediate cost to the farm sector decreases but the overall cost to society of achieving the reductions sharply increases. This reflects the fact that a uniform tax on all emissions is society’s most cost-effective strategy if other issues, such as competitiveness, leakage, and social balance are ignored. If we take account of these other criteria and limit the immediate cost to the agricultural sector, there is a lower production decline and therefore a corresponding need for additional subsidies for technical reductions, which increases the socio-economic cost indicated by the shadow price.

When a CO2e tax is introduced, the CO2e reductions can be separated into two types of reductions: structural effects and other effects. Structural effects represent emission reductions arising from a reduction of or changes in production. Where there are large structural effects there is an increased risk of leakage (where emission reductions in Denmark are offset by increased production and emissions outside Denmark). The term ‘Other effects’ in Table 2 covers both technical effects (reductions that do not affect the scope of production but reduce emissions per unit produced) and the impact of complementary activities (e.g. change from agricultural land to forest and the re-wetting of carbon-rich agricultural soils). There is no hard-and-fast separation between these two categories: the adoption of a mitigation technology such as a feed additive may be costly, so in addition to reducing emissions per unit of output it may also lead to reduced output. However, in principle the production effects are aggregated and entered under structural effects, while the reduction in emission intensities is included as an ‘other effect’.

Table 2 shows, unsurprisingly, that the structural effects are largest with the most ambitious Model 1. Other effects are more important both relatively but also in absolute terms in Models 2 and 3, reflecting the assumed greater role of biochar in achieving the targeted reductions. This division between structural and other effects, and indeed the overall reductions achieved, are dependent on the mitigation technologies included and captured in the model and their associated costs. The GreenReform model assumes that only a limited range of technologies would be attractive for farmers to adopt even with a carbon price of DKK750/EUR100 per tonne CO2e. For livestock farmers, only two technologies are assumed to be relevant, feed additives and adding a cover to slurry tanks (and even here there is doubt whether the use of feed additives will be possible for organic producers) while no technical options are relevant to reduce emissions per unit of fertiliser (the cost of nitrification inhibitors is estimated to be much higher than DKK750/EUR100 per tonne CO2e).

The cost of emission reductions with biochar is estimated to be between DKK900-3,300/EUR120-440 per tonne, but it is assumed that biochar use (if allowed) will be subsidised through the special fund created for this purpose. Recall that measures such as cover crops and set-aside that contribute to increased soil carbon sequestration are not relevant as changes in soil carbon content are not covered by the proposed taxation system (apart from rewetting organic soils). Still, it should be kept in mind that measures included in other climate action plans, such as animal genetics (breeding for low-methane animals), animal health interventions (improving the productivity of animals) or multi-species swards (to reduce fertiliser use) have not been formally considered, even if these longer-term interventions are unlikely to yield significant reductions in the short term.

An argument often used to support a carbon tax is that it raises revenue that can be recycled back to farmers. Table 1 shows the net revenue impact on the public finances for the different models. The revenue impact is calculated after changes in farm behavior and the effect of the feedback effects on the state’s other income and expenses have been taken into account. Only in Model 1 is there a positive net revenue after agriculture has adapted to the tax, once the need to subsidise the additional afforestation and the rewetting of organic soils is taken into account.

The immediate cost to agriculture (which is the mirror image of the revenue collected by the tax) is estimated at DKK5.9 billion in Model 1. But farmers will adjust their production activities to minimise their tax exposure, and after these adjustments the revenue falls to DKK3 billion. However, DKK1.8 billion is needed to pay for afforestation and the rewetting of organic soils, leaving just DKK1.2 billion as net revenue for distribution. The Expert Group suggests that this net revenue can be returned to the industry in the form of a support pool for testing and conversion to new climate-friendly agricultural technologies and/or for conversion support in the form of state compensation for relevant green investments. In the other two models, there will be a need for additional state financing particularly given the need to incentivise biochar use. The absence of revenue from the carbon tax to recycle back to farmers may reflect the particular features of the Danish situation where a significant part of the revenue is already earmarked to subsidise afforestation and the rewetting of organic soils.

Carbon leakage

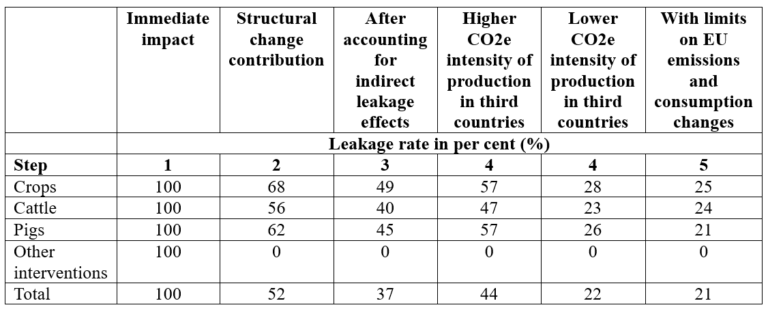

Carbon leakage can occur if reduced production in Denmark is replaced by increased production outside of Denmark, either in other EU countries or in third countries. Emissions would increase outside of Denmark partly or even wholly substituting for the reduction brought about by a CO2 tax on Danish agricultural emissions. Carbon leakage can be expressed as a leakage rate, calculated as the emissions increase outside the country implementing a climate policy divided by the emissions decrease in the implementing country (see Matthews, 2022 for further discussion of carbon leakage). The GreenReform model has a leakage module which allows the Expert Group to come up with estimates of the leakage rate associated with each of its models, although it notes that its estimates are subject to significant uncertainty. The module has a 5-step approach which is first explained, after which the leakage rate estimates for the various models are shown.

The five steps in the calculation of leakage rates are the following.

- Step 1 assumes that there is no difference in the emissions intensity of Danish and third country production, no technological reduction possibilities, and that Danish production is substituted 1:1 by production in third countries. Under these assumptions, the leakage rate is 100%.

- Step 2 allows for emissions reduction through technological mitigation, so only the structural effect (defined previously) which captures reduced production contributes to leakage. In Model 1, the structural effect accounts for 52% of emissions reductions and thus the leakage rate reduces to 52%.

- Step 3 take account of indirect leakage, whereas Step 2 only accounts for direct leakage. Indirect leakage effects arise through general equilibrium effects in both Denmark and third countries (resources shift between sectors with different emissions intensities, and the introduction of the Danish tax results in a small fall in global production and thus emissions). This indirect effect is calculated to reduce the leakage rate further to 37% in Model 1.

- Step 4 relaxes the assumption that emission intensities of agricultural production in Denmark and third countries are the same. As there is considerable uncertainty about relative emission intensities, the Expert Group report makes a sensitivity analysis assuming that Danish production is both more emissions-efficient but also less emissions-efficient than production in other countries. Depending on the assumption, the leakage rate is either increased to 44% or reduced to 22% in Model 1.

- Step 5 uses relative emission intensities for Danish and third country agricultural production from a specific data source (the GTAP-E model), adds the assumption that increases in agricultural production in other EU countries will be limited if they are to live up to their obligations under the Effort Sharing Directive, and also allows for consumption changes in response to the higher price of emission-intensive commodities. With these assumptions, the leakage rate in Model 1 falls to 21%.

The Expert Group notes that the leakage rates will differ for the individual sectors in Danish agriculture due to differences in each of these assumptions – the share of emission reductions contributed by structural effects, the impact on indirect leakage, relative differences in emission intensities with production in third countries, and the behavioural responses of consumers to higher prices. Table 3 shows anticipated leakage rates by sector for Model 1 in 2030.

Table 3. Leakage rates with Model 1 by agricultural sector in 2030

Source: Expert Group on Green Tax Reform, final report, February 2024.

Table 4 summarises the leakage rates estimated with the GreenReform model for all three models. The ranges given correspond to the estimated leakage rates in Steps 3-5 in each case. The calculated leakage rate falls from Model 1 to Model 3. This reflects the lower effective tax rate and thus a lower production reduction, and a greater contribution from technical mitigation that does not contribute to leakage.

Table 4. Leakage rates associated with each model in 2030

Source: Expert Group on Green Tax Reform, final report, February 2024.

Carbon leakage can be reduced by reducing the amount of the CO2 tax (as shown by comparing Models 1 and 3) and by introducing compensation mechanisms. The Expert Group points out that it has recommended rebates in several of its models which lower the effective tax rate while maintaining the marginal incentive effects. It also highlights that in its Models 2b and 3b it proposes to substitute a tax on fertiliser use by an incentive subsidy mechanism financed by repurposing CAP direct payments. This would also lower fertiliser emissions with a significantly lower hit on agricultural production but with some reduction in effectiveness and at a higher social cost. Finally, it references the possibility of additional conversion support for farmers who might wish to transition their farms to less emissions-intensive production, for example, by converting from animal to crop production.

Carbon leakage can also be reduced if other countries introduce similar policies to price agricultural emissions. From a Danish perspective, it would be desirable to see the introduction of an EU-wide tradable allowance system which would impose a uniform CO2 charge on agricultural production and create equal conditions of competition (to the extent that production is more emissions-efficient in a country like Denmark, it could even give a competitive advantage to Danish producers). In the context of setting the EU’s 2040 climate target, the Expert Group supports the Danish government’s position to advocate for an EU-wide tradable allowance system. The Expert Group does not advocate that this would make the Danish CO2 tax redundant. Instead, as for industries covered by the ETS, it proposes that the Danish CO2 tax would be reduced by the allowance price in an EU agricultural ETS (AgETS). What this concretely might entail would depend on the Danish government’s climate target, the level of allowance prices in an AgETS, and the size of the rebate that industries covered by the ETS would be given in future.

Price and income effects

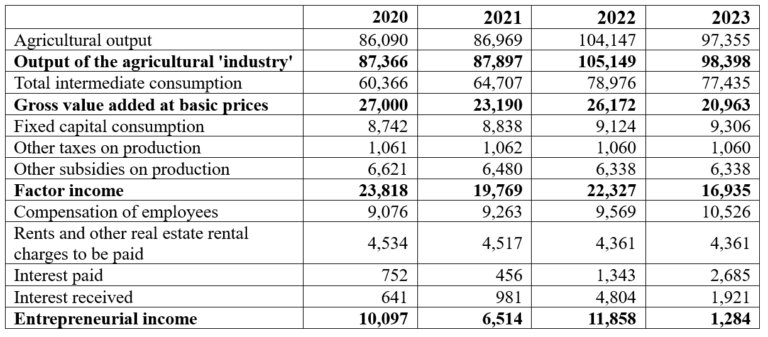

Of particular interest is the likely impact of a carbon tax on the value added and income arising in the agricultural sector. Table 5 gives the relevant background data. Danish agriculture is extremely intensive as shown by the very high ratio of intermediate consumption to agricultural output. This means that factor income and particularly entrepreneurial income are very sensitive to small changes in either output or input values. The immediate impact of a CO2 tax in Model 1 is estimated as an additional cost of DKK 5.9 billion (see Table 2 previously). If this were the final cost, it would clearly levy a very large additional burden on Danish agriculture.

Table 5. Economic accounts for Danish agriculture, DKK million.

Source: Eurostat, Economics Accounts for Agriculture domain acct_eea01.

However, this immediate burden is significantly reduced by the behavioural and market adjustments that take place following the introduction of the tax. The Expert Group does not provide a table similar to Table 5 giving an estimate of the post-tax income arising in the sector. Instead, it presents the income impact in terms of the projected fall in land prices. As land prices reflect the earning potential of land, this can be taken as a proxy for the expected fall in the income arising in agriculture following the introduction of the tax. (In the model land prices are related to a net margin concept (Dækningsbidrag II) which subtracts variable and partially variable costs from the value of output. Area-based direct payments under the CAP, apart from environmental payments, are not taken into account). The projected fall in land prices in Model 1 is 16.8% but when the subsidy for diversification into forestry is accounted for, this fall in land prices is reduced to 8.8%.

This implicit fall in net margin (as a proxy for income arising in agriculture) is much smaller than what might be anticipated just by looking at the immediate burden on the sector, for two main reasons. First, farmers themselves adjust to the new tax, either by adopting technical mitigation options that are now economically profitable, by reducing production of more emission-intensive enterprises or by switching to enterprises with lower emissions. These adjustments alone reduce the tax bill on agriculture from DKK 5.9 billion to DKK 3.0 billion in Model 1, although this reduction will be partly offset by the additional cost of the technical options, such as feed additives to reduce methane emissions from cattle.

The other important mechanism is the ability of the sector to shift some of the burden of the remaining tax to consumers. The reduction in production following the introduction of the tax means that producer prices increase. According to the GreenReform model calculations, in Model 1 fully 56% of the tax bill will be shifted to consumers, reducing the burden on the agricultural sector to DKK 1.7 billion plus the cost of the mitigation technologies. Especially when new opportunities for diversification open up through the massive increase in the subsidy for afforestation, the negative impacts of the tax on the Danish agricultural sector are greatly attenuated.

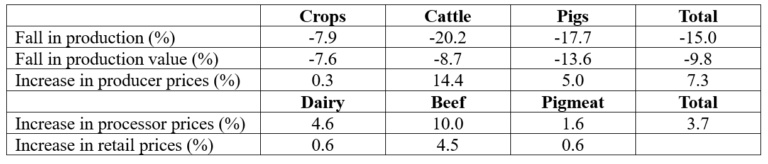

The price changes projected by the GreenReform model are shown in Table 6. Overall, the estimated 15% fall in production is projected to lead to a 7.3% increase in average producer prices, though the producer price increase varies across commodities. For pigmeat, the increase is 5.0% while for cattle (which in Denmark is mainly dairy production) the increase is much higher at 14.4%.

Table 6. Changes in production and production value in 2030 – Model 1

Note: The increase in producer prices is calculated as (100 + fall in production value)/(100 + fall in production) where these values enter with a negative sign.

The retail price change for dairy is calculated for 1 litre milk; for beef for 500 gm minced beef; and for pork for 500 gm minced pork.

Source: Expert Group on Green Tax Reform, final report, February 2024.

The producer price response to a decrease in supply is determined primarily by the price elasticity of demand in both domestic and export markets. Lower price elasticities of demand, which reflect some degree of market power (for example, a branded butter with loyal customers), will lead to higher price increases, and conversely. The Danish animal sectors are very export-oriented, with around two-thirds of dairy products exported and almost 90% of pig production. The Danish agricultural sector argues that the export elasticities used in the GreenReform model are too low (see the report commissioned from Copenhagen Economics on this topic). They argue that the degree of competition on export markets is such that the ability of processors to pass on the price increases shown in Table 6 to their export customers is greatly over-estimated by the elasticities used in the model. They argue, as a result, that a much higher share of the burden of the tax will fall on the agricultural sector. The Expert Group has conducted a sensitivity analysis and concluded that using a higher export elasticity would have little impact on the overall results. For example, doubling export elasticities would reduce the share of the tax bill that can be shifted to consumers through higher prices from 56% to 47% in Model 1.

Conclusions

The report of the Expert Group on Green Tax Reform in Denmark is to date the most detailed investigation of the impacts of introducing a price on agricultural emissions in a single country. The GreenReform model on which it is based has been under development for five years, and is now widely seen as the most advanced model of its type to simulate the environmental and climate impacts of changes in the economy and public policies.

Several conclusions from the report are generally relevant while others derive more from the specific challenges and starting point for reducing agricultural emissions in Denmark. The most important conclusion is that introducing a farm-based emissions price is both feasible to implement and effective in operation. Related to this conclusion is that introducing a price on agricultural emissions inevitably leads to trade-offs between the different objectives to reduce emissions in the most cost-effective way, while minimising any loss of competitiveness for the agricultural and food processing industries, avoiding any additional burden on the public finances, while maintaining social balance between different regions and different income groups. The Expert Group argued that deciding between these different objectives is ultimately a political choice, but it provided a range of different models that considered different weightings for these different objectives. These included reducing the nominal tax rate, lowering the effective tax using rebates, proposing a subsidy model for fertiliser rather than a levy model to be financed from CAP funds, or mandating the use of specific technologies through regulation.

The Expert Group recommended to price agricultural emissions using a carbon tax rather than an emissions trading scheme. This may limit its relevance to the discussion starting within the EU on how agriculture can best contribute to meeting the EU’s 2040 climate target. Here, a carbon tax appears to have been ruled out a priori given that it could only be introduced if all Member States agree. But faced with the many advantages of a carbon tax compared to the complexities of including agriculture within a trading scheme (an AgETS) it is very possible Member States could be persuaded to support a carbon tax knowing that an emissions trading scheme would be introduced in any case.

Important quantitative findings from the report are that there can be significant carbon leakage from implementing a unilateral carbon tax in a single country (estimated rates of between 40-60% for sectors covered by the tax assuming that Danish agriculture is at least and probably more emissions-efficient than its competitors), but that price impacts on consumers are minimal. The tax is also effective. With estimated emissions from animal and crop production in 2030 of 10.1 Mt CO2e, a tax of EUR 100/t CO2e is projected to reduce these emissions by 2.7 Mt CO2e or by 27% by 2030 if introduced in 2027, with a further 0.5 Mt CO2e coming from rewetting of organic soils and afforestation funded by the proceeds of the tax revenue.

The report has been criticised for its heavy reliance in those models where the tax rate is reduced on the adoption of biochar to achieve the required cut in agricultural emissions. It admits that environmental approval for storing biochar in soils has yet to be given, that the capacity to produce biochar in the required quantities is not yet in place, and that the sequestration effects of biochar are not yet recognised for the purposes of the national inventory. These obstacles can be overcome but they will take time.

The report was delivered to government in February 2024. In the previous December, the government had established a tripartite commission consisting of the main farm organisation, the main nature conservation organisation, representatives of industry, trade unions and local municipalities. The broad terms of reference (in Danish) of this commission are to develop an agreed strategy for the green transition in Danish agriculture and how best to manage land use, nature and water resources. Specifically, it has been tasked to come up with concrete recommendations for how a CO2 tax on agricultural emissions should be designed in the light of the recommendations of the Expert Group. The commission has until June 2024 to deliver its report.

The government’s hope is that the various interests in the commission can converge on a common proposal. This would then make its job of implementing this proposal super easy. But it is just as possible that a common agreement will not be reached, throwing the ball back to the government to make the decision. For this reason, it is a tense time in Danish agricultural politics just at this moment.

This post was written by Alan Matthews (CAP Reform); TAPP Coalition added the remark and the weblink on a tax on beef and dairy